Some Weeks the Impossible Happens

A week that felt like a year: the U.S. and Iran reached a peace deal that reopened the Strait of Hormuz, sending oil and inflation lower just as Kevin Warsh chairs his first FOMC meeting. SpaceX completed the largest IPO in Wall Street history and unveiled AI1, its first orbital data center, the same week Oracle posted a $638B backlog and a clean Q4 beat. The throughline: AI infrastructure is sorting into three permanent layers, space, cloud, and on-premises, each with a natural founder-led owner, leaving the commodity hyperscaler middle facing a structural squeeze.

Opening Bell: Some weeks the impossible happens.

There are weeks that feel like years. This was one of them. Welcome to Issue #5.

The New York Knicks won the NBA Championship for the first time in 53 years. The United States and Iran agreed to a peace deal, reopening the Strait of Hormuz and triggering a cascade of consequences for oil, inflation, and the Fed. SpaceX completed the largest IPO in Wall Street history and unveiled AI1, the world's first orbital data center. And the AI infrastructure stack sorted itself into three permanent layers, each with a natural founder-led owner, leaving the non-founder-led commodity middle facing an inescapable structural squeeze.

We build the Founders 100 ETF (FFF) because founders are built for a world moving at the speed of light. Founders think in decades, not quarters. They see around corners and beyond the stars.

Kobe Bryant once sat in a postgame press conference after winning a championship and told the world he wasn't satisfied. Job not done. That is Founder DNA, and it captures the spirit of our 30-year journey ahead, both as your market guides and as top FFF shareholders fully aligned and invested alongside you.

Michael Monaghan, Founder & Portfolio Manager, Founders 100 ETF (FFF)

Founder Spotlight

Elon Musk at SpaceX (SPCX)

The generational thesis behind our newest position.

The Founder

Elon Musk is the defining founder of our generation. He taught himself rocket science, nearly went bankrupt three times, and on the fourth and final possible launch of Falcon 1, he succeeded. Today SpaceX is the largest IPO in Wall Street history, debuting on Nasdaq with an opening trade of $150 per share and a $1.77 trillion valuation. This is what founders do: they turn audacious goals into trillion-dollar realities.

The Business

Starlink crossed 10 million subscribers in February 2026, adding up to 1.5 million new users per month, with the connectivity segment already posting $1.19 billion in profit last quarter and growing.

The Orbital AI Thesis

As we told Charles Payne on Fox Business, most investors miss the scale of what SpaceX is building in space. Reusable Starship launches turn orbital data centers into the lowest-cost commodity compute on or off Earth. Heat dissipates freely in the vacuum of space, meaning no cooling bills and no water use. Solar panels capture sunlight 24/7, delivering roughly 5× the energy density of terrestrial panels, which go offline at night. At a time of energy scarcity and soaring power costs, this is a structural advantage terrestrial competitors simply cannot match.

SpaceX's AI1 orbital data center targets 1 GW of orbital compute by late 2027, scaling by an order of magnitude annually. The long-term vision: one million satellites, 100 GW of AI compute, powered entirely by the sun. The demand is already here, with Anthropic and Google paying SpaceX nearly $2 billion per month combined for AI compute capacity.

The Closed-Loop Moat

SpaceX owns the full stack: its own chips via Terafab, Grok AI models from the xAI merger, global internet via Starlink, the rockets, and Tesla robotics integration. Data feeds AI, AI optimizes hardware and launches. No one else on Earth or in orbit has this one-of-a-kind flywheel. It's not a moat; it's a canyon.

Our Position

We established a 1% position for FFF shareholders on the opening trade at $150 per share. We are long-term holders, not traders. As insider selling through year-end puts downward pressure on the stock, we will watch it closely, because we believe the thesis only gets stronger as each Starship launch, AI1 deployment, and Terafab milestone compounds.

We believe SPCX belongs in the conversation alongside the great founder-led compounders of the last century. The future is shaped by founders, and SpaceX is building the infrastructure for the next fifty years.

A Stat That Travels

100%

We believe founders are a different breed, and the data proves it. With skin in the game, they think in decades, not quarters, and build with the drive of someone who refuses to let what they created become ordinary. Bain & Company found founder-led S&P 500 companies outperformed their peers by 3× over 25 years and 2× over the past decade. SPY gives you 17% founder exposure, QQQ 21%, FFF 100%. Hired CEOs manage. Founders build what lasts.

Source: Source: Bain & Company analysis of companies in the 2014 S&P 500; indexed total shareholder return from 1990 to 2014.

Industry Insight

The AI Infrastructure Race Across Earth and Orbit

The AI infrastructure buildout is the largest capital investment cycle in the history of technology, and this week delivered three defining data points simultaneously: SpaceX completed the largest IPO in Wall Street history, Oracle reported a $638 billion RPO, and the potential Strait of Hormuz reopening threatened to reprice the energy costs underpinning every data center on Earth.

The Numbers

Oracle secured over 10 GW of data center capacity coming online over three years, is spending $50 billion on AI infrastructure in 2026 alone, and grew AI infrastructure revenue 243% year-over-year. SpaceX debuted at a $1.77 trillion valuation, with anchor customers already paying nearly $2 billion per month combined for compute capacity. AI1 prototypes launch in early 2027.

The Stack Is Settling

We believe one of the most important structural shifts in technology investing is quietly taking shape, and the market hasn't fully priced it yet. The AI infrastructure buildout is sorting itself into three distinct layers. Each has a natural owner. The companies caught in the middle face a squeeze that we believe will compress multiples even as revenues continue to grow. Capital is flowing to the edges fast: Dell's private AI business is accelerating, and Oracle is already permitted for three small modular nuclear reactors to power its next gigawatt campus.

| Layer | Winner | Use Case | Moat | Vulnerable To |

|---|---|---|---|---|

| Space Cloud | SPCX | Collective AI, general inference, batch processing | Free solar power, no land/water/permits, infinite scale | Early-stage, unproven economics |

| Earth Cloud | ORCL | Private enterprise & government, sovereign data | Trust, compliance, data residency, RPO $638B | Nothing near-term |

| Earth On-Premises | DELL | Military, HIPAA, regulated, air-gapped | Physical control, zero connectivity requirement | Nothing near-term |

| The Squeeze | AWS / Azure / GCP | Commodity public cloud | Switching costs only | SPCX from below, ORCL from above |

Layer One, Space Cloud: SpaceX's AI1 orbital data center targets collective AI workloads: foundation-model training, general inference, and latency-tolerant batch processing. The economics are compelling: no land, water, night, or permits, and solar power and vacuum cooling are free at scale. SpaceX targets 1 GW of orbital compute by late 2027, scaling by an order of magnitude annually thereafter.

Layer Two, Earth Cloud: Oracle's $638 billion remaining performance obligation isn't an accident. Enterprises and governments have data they will never put in space: proprietary models, patient records, financial transactions, sovereign intelligence. You cannot run a classified DoD workload on a private satellite constellation. You cannot satisfy GDPR data-residency requirements when your data orbits over seventeen jurisdictions per hour. Oracle wins this layer not by being cheapest, but by being trusted.

Layer Three, Earth On-Premises: Dell's private AI infrastructure serves the most sensitive workloads of all: air-gapped military systems, HIPAA-regulated hospital records, and proprietary enterprise AI that never leaves the building. No cloud, terrestrial or orbital, competes here.

The Squeeze

That leaves AWS, Microsoft Azure, and Google Cloud in what we believe is becoming a commodity middle, attacked simultaneously from below by cheaper orbital compute and from above by stickier private infrastructure.

AWS is most exposed, with no proprietary frontier AI model, no enterprise software moat, and its largest customers simultaneously its AI suppliers and potential defectors to cheaper orbital compute.

Google faces a paradox. It has arguably the best AI models of any hyperscaler, yet is reportedly paying SpaceX ~$920 million per month for xAI compute, funding the competitor. Google may ultimately become a model and software layer sitting atop space infrastructure rather than owning the compute itself.

Microsoft is the most defensible. Office 365, Teams, Active Directory, and GitHub Copilot create genuine switching costs. But we estimate roughly 40–50% of Azure workloads are pure compute, not Office-adjacent, and those workloads are exactly what orbital repricing will target first.

Energy Is the Binding Constraint, For Now

Every data center conversation comes back to power. The Strait of Hormuz reopening doesn't just move oil; it reprices the energy-cost assumptions embedded in every terrestrial data center's operating model and shifts the cost comparison between orbital and terrestrial compute. It is the most underappreciated industry catalyst of 2026.

The Historical Analogy

This rhymes with cloud vs. on-premises. Conventional wisdom said cloud would kill on-premises. Instead, total compute spending expanded and both layers grew. We believe space compute follows the same pattern, expanding the total addressable market rather than cannibalizing terrestrial. The real disruption is a permanent structural sorting that leaves the commodity middle without a defensible moat.

| Milestone | Timeline | Significance |

|---|---|---|

| SpaceX AI1 prototypes launch | Early 2027 | Proof of concept; 1 GW orbital target |

| AI1 becomes commercial | ~ 2028 - 2029 | Orbital cost data goes public; repricing begins |

| Hyperscaler multiple compression | 2029 - 2031 | Growth premium erodes even as revenues hold |

| Oracle & Dell rerating | 2028+ | Market recognizes permanent lane ownership |

What We're Watching

Starship's launch cadence is the variable no analyst has fully modeled. Every successful flight compresses the orbital compute cost curve faster than consensus expects. Oracle's nuclear SMR timeline and Dell's enterprise AI pipeline are the terrestrial counterweights. The critical inflection point arrives when SpaceX's AI1 prototypes become commercial, roughly 2028 to 2029; that is when orbital cost data becomes public and repricing of commodity hyperscaler workloads begins in earnest.

Until then, we believe Oracle and Dell represent structurally underappreciated positions in the AI infrastructure stack, not as bridge holdings, but as permanent owners of the layers that neither space nor commodity cloud can serve. Founders build infrastructure that lasts, and we believe the companies with the clearest lane in this three-layer world are the ones worth owning for the next decade.

Portfolio Pulse

Founders in Their Own Words

Our take. Astera Labs (ALAB) is the AI data center's nervous system. Co-founders Jitendra Mohan, Sanjay Gajendra, and Casey Morrison quit their jobs at Texas Instruments to start Astera in a garage, with a singular mission: eliminate the connectivity bottlenecks choking AI infrastructure. They were just named EY World Entrepreneur of the Year 2026, the fourth US winner in the award's history. The business has earned it: revenue and EPS have grown more than 5× since IPO, with Q2 2026 guidance of $355–$365 million reflecting 15–18% sequential growth.

Our take. CoreWeave (CRWV) is the GPU cloud built by founders for the AI era. Co-founder and CEO Michael Intrator has led CoreWeave since its founding in 2017, and his playbook is classic founder: prioritize scale over near-term profit. Intrator has said CoreWeave could turn profitable within three months if it stopped scaling, but the generational opportunity of ramping AI infrastructure is the priority. The company reached $5 billion in revenue faster than any cloud platform in history, growing 168% year-over-year.

Our take. Nebius Group (NBIS) is a founder's second act. Arkady Volozh co-founded Yandex and ran it as CEO for 25 years before building Nebius into one of the largest independent AI infrastructure providers. He separated Yandex's non-Russian assets, built a legitimate GPU cloud platform from scratch, and counts Nvidia as a $2 billion strategic investor, with compute infrastructure running across Europe and the US. Up 165% year-to-date, the market is beginning to understand what he's building.

Our take. Rocket Lab (RKLB) is the space infrastructure play that complements our SpaceX thesis. Founder Sir Peter Beck started Rocket Lab in New Zealand in 2006 and built it into the leading small-satellite launch provider, the Electron to SpaceX's Falcon. As the orbital compute buildout accelerates, launch cadence is everything, and Beck owns the second lane.

Conviction Corner

RIA Q&A on FFF's Role in a Portfolio

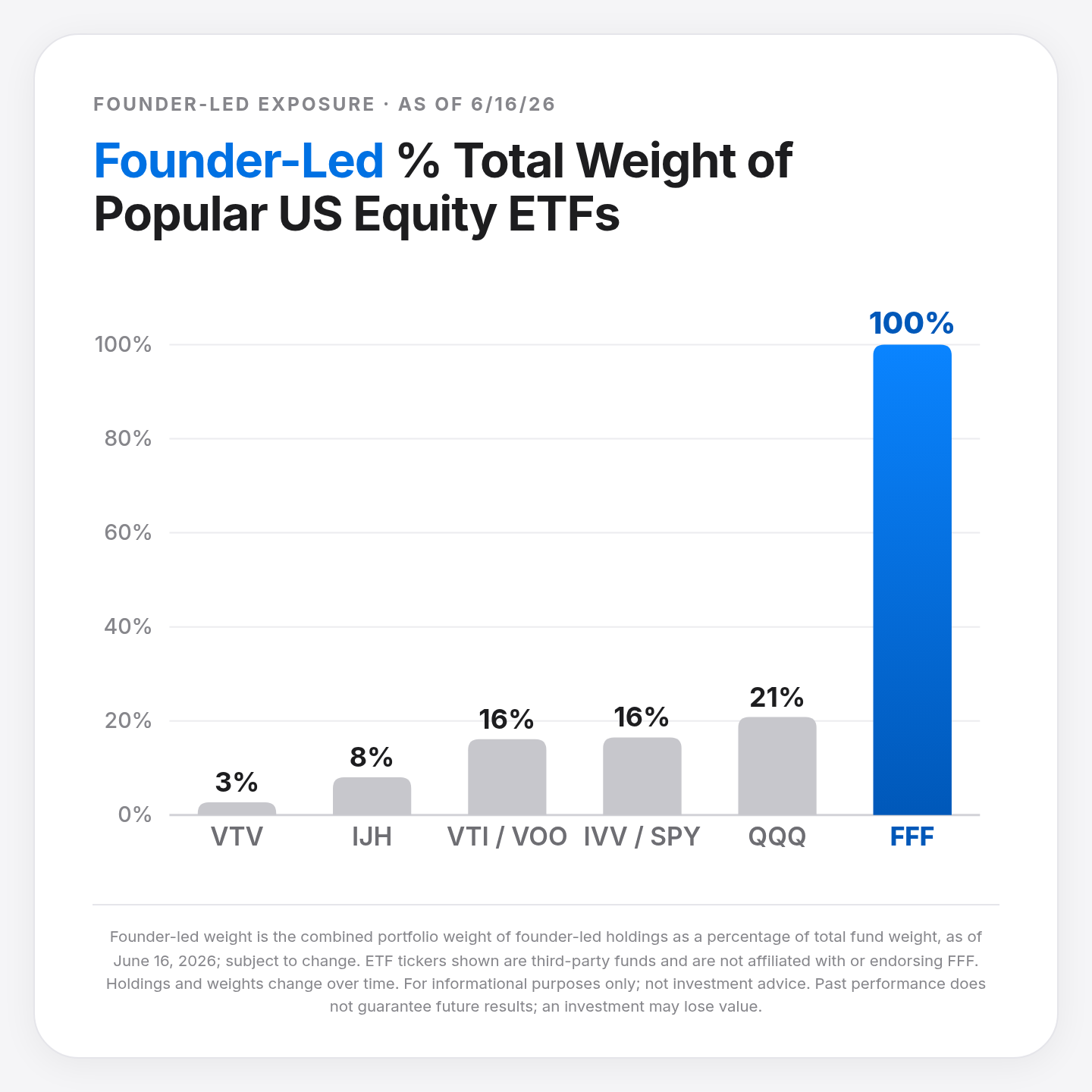

Don't my clients already own founders through SPY and QQQ?

Q. My clients already own SPY, QQQ, or VOO. Don't they already have exposure to founder-led companies?

A. Less than you might think. The most popular US equity ETFs by assets under management carry surprisingly little founder-led exposure. SPY, VOO, and VTI sit at just 16%, QQQ at 21%, and VTV at 3%. FFF is 100% founder-led by design. The bar chart below tells the story better than any words can.

Macro Minutes

U.S. Economic Releases · June 16 - 20

What We're Watching

Tue, Jun 16: Retail Sales + FOMC Begins

May retail sales drop Tuesday alongside the start of what we believe is the most consequential Fed meeting since 2022. Kevin Warsh likely chairs his first FOMC meeting this week, with updated economic projections and the dot plot giving markets the first read on the new Chair's rate path. No rate cuts are currently priced for 2026; bets for a hike are rising. A soft retail number complicates that hawkish consensus.

Wed, Jun 17: FOMC Decision + Press Conference.

The rate decision drops at 2:00 PM ET. We believe the Fed holds at 3.50%–3.75%. The more important signal is the dot plot: does the median projection shift to price in a hike by year-end? Warsh's first press conference sets the tone for the back half of 2026.

Tue, Jan 16 – Wed, Jan. 17: Housing Starts + Industrial Production.

Two additional reads on an economy navigating tariffs, energy inflation, and geopolitical uncertainty simultaneously.

Earnings Edge

1 FFF Holding Reporting This Week

Larry Ellison, Founder & CEO

Q4 FY2026 · just reported

Oracle delivered a clean Q4 FY2026 beat: sales of $19.2B (+21% YoY) and adjusted EPS of $2.11 (a +8%, or +16-cent, beat), driven by IaaS growth of +93% and total cloud revenues hitting $9.9B (+47% YoY). RPO climbed to $638B, up $85B sequentially, fueled by large-scale AI contracts where customers prepaid for GPUs or supplied their own hardware, reducing Oracle's capital burden on those deals. Operating margins rose to 45%, indicating that ORCL is pricing its new business correctly. Management guided FY2027 revenue growth of +34% with non-GAAP EPS of $8.05 and Q1 cloud growth of 58–64%, even as near-term margins face pressure from an aggressive data center buildout, a classic Ellison founder move: bet the balance sheet early, absorb the pain, and convert $638B in backlog into high-margin revenue as capacity comes online. The stock traded down on concerns about the big capex spend, but the quarterly results strengthened our thesis that Ellison will execute. Larry saw the AI opportunity in 2023. After 49 years of reinventing Oracle ahead of every major technological wave, five in all, we fully trust his AI capex plans and think the business will pivot strongly into free cash flow in 2029 and not look back. We are patient and hold high conviction in our three-year thesis on ORCL.

Washington Wire

The U.S. - Iran Peace Deal Is Done.

“Following intensive talks, we are pleased to announce that the Peace Deal between the United States of America and Islamic Republic of Iran has been REACHED. Both sides have declared the immediate and permanent termination of military operations on all fronts, including in Lebanon.”

Shehbaz Sharif, Prime Minister of Pakistan and lead mediator, June 14, 2026:

Our take. It's done. After months of conflict, a Strait of Hormuz blockade, Khamenei's end, and a morning that nearly saw the deal break apart over Israeli airstrikes on Beirut, peace was reached. The market implications are large, immediate, and cascading. The Strait of Hormuz, where ~20% of global oil flows, is open. Oil prices are falling, inflation is cooling, lower-income consumers feel relief at the pump, and the Fed has one less reason to hike rates at this week's FOMC meeting, creating a powerful tailwind for US growth stocks, led by our founders. Also benefiting FFF: cheaper energy compresses data center operating costs, accelerates AI infrastructure buildout timelines, and reduces input-cost pressures across our industrial and consumer holdings. The May 4.2% CPI print, driven overwhelmingly by energy, may prove to be the peak of this cycle. "Higher for longer" becomes "soft landing achieved." The harder work of governance and reconstruction now begins, and whether the deal proves durable remains to be seen. We will be watching closely, but today the guns are silent, oil is falling, and the macro backdrop for our founders just materially improved.

Not investment advice. Past performance does not guarantee future results. Investors should carefully consider FFF's investment objectives, risks, charges, and expenses before investing. The prospectus contains this and other important information. Read it carefully before investing at: FounderETFs.com/FFF Distributed by Vigilant Distributors, LLC.

The data presented reflects Founder-Led company weightings as of 5/28/26 and is subject to change without notice. Founder-Led weighting is determined by if a company's original Founder currently serves as a chief officer (e.g. CEO, CTO).

Comparison to other ETFs (VGT, IWF, VUG, XLK, QQQ, IVV, SPY, SPYM, VTI, VOO, IJH, VTV) is for informational purposes only and does not imply that FFF will outperform any listed fund. Different ETFs have different investment objectives, strategies, risks, charges, and expenses. Holdings and weightings change frequently and may differ materially at the time of reading.

A higher concentration in Founder-Led companies does not guarantee superior performance and may introduce additional risks, including key-person risk, governance risk, and concentration risk. Not a solicitation to buy or sell any security.

Founder Factor · Weekly Newsletter