Where's the inflection? This week: Memory.

Every AI buildout story eventually runs into the same wall: how fast a chip can move data, not just process it. That bottleneck has put memory, once the most commoditized corner of semiconductors, at the center of the AI infrastructure debate. The Founders we follow most closely aren't the ones making memory chips. They're the ones whose entire business models depend on solving the bandwidth problem memory creates.

Founder Spotlight

Jitendra Mohan at Astera Labs (ALAB)

The traffic controller inside the AI factory.

Jitendra Mohan co-founded Astera Labs (ALAB) in 2017 to remove the connectivity bottlenecks choking modern data centers. GPUs are only useful if they can access memory fast enough. Astera Labs builds the connective tissue between GPUs (the muscle of AI), CPUs (the brain of AI), and high-bandwidth memory; the unglamorous but essential plumbing that determines whether an AI cluster actually performs at the speed its chips are capable of.

Think of Astera Labs as the traffic controller inside an AI factory. As clusters scale from thousands of GPUs to millions, every additional chip adds more cross-talk, more retiming, more places for a signal to degrade before it reaches memory. ALAB's platform sits directly on the standards driving that scale-up, including CXL (the protocol that lets CPUs and GPUs share memory) and PCIe Gen6 (the highway connecting chips inside a server), and benefits any time a hyperscaler moves to rack-scale AI architecture. The bigger and more memory-intensive AI factories become, the more connectivity becomes as important as compute itself.

This is exactly the kind of company most ETFs miss. It's Founder-Led, technically differentiated, and sitting on a secular tailwind that doesn't depend on picking which AI model wins. As long as clusters keep getting bigger, the traffic controller stays busy.

Industry Insight

A Structural Reset, Not a Memory Cycle

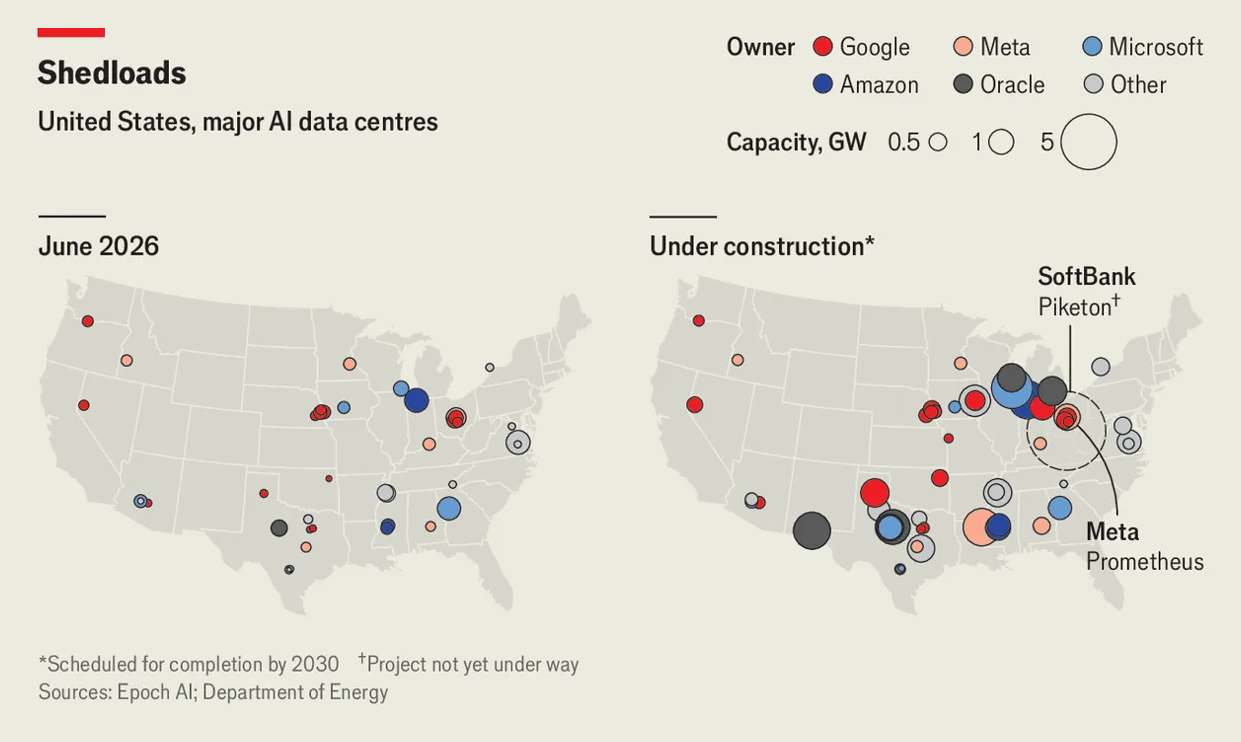

Memory capacity additions are running years behind demand projections, and switching costs for hyperscalers locked into long-term supply agreements are high. That dynamic favors incumbents with existing capacity commitments over new entrants, regardless of how compelling a competitor's chip design looks on paper. The map above makes the demand case visually: the cluster of data centers already operating across the US is striking, but the "under construction" map is the real story. The density of new builds, anchored by Oracle's massive Texas footprint and Meta's Prometheus project, tells you why HBM supply is sold out through 2026. Every one of those circles needs memory to function.

Map: The Economist

Memory has historically been the most notoriously cyclical corner of semiconductors, lurching between shortage and glut roughly every two to three years. Consensus still largely expects that pattern to reassert itself, with most analysts penciling in some easing of the current HBM bottleneck within the next 18 months as new capacity from Samsung, SK Hynix, and Micron comes online.

Our thesis. Memory is undergoing a structural reset, not a typical cycle, and the data backs us. AI training and inference demand is compounding faster than new capacity can be added, with model sizes growing ~10x per year and inference scaling even faster as applications move into production. HBM demand is projected to grow >70% YoY through 2026 after 130% the prior year, making a quick oversupply unlikely. Once hyperscalers lock in an HBM generation, the architecture stays for the full lifecycle, giving suppliers rare multi-year visibility. This structural tailwind strongly favors the Founder-Led leaders in our Founders 100 ETF (FFF) portfolio.

None of this eliminates cycles entirely. Pricing will still swing with new fab ramps and generational transitions, and some analysts flag potential HBM price pullbacks later in 2026 as competition rises. But swings should be smaller and shorter-lived, with a rising demand floor from expanding AI workloads. This is a meaningfully different setup than the classic boom-bust memory cycle, which is why we believe the consensus "18-month bottleneck resolution" view is too tidy.

Portfolio Pulse

Founders in Their Own Words

“The frontier models driving today's most demanding AI applications require connectivity infrastructure that keeps pace with the accelerators powering them.”

Our take. Mohan is describing a market where connectivity is the bottleneck. As AI clusters scale to millions of chips, the "traffic controller" becomes as valuable as either the GPUs (muscle) or CPUs (brain).

“We are not designing a chip. We are designing an entire infrastructure all at once. NVIDIA is the only company in the world today where you can give us a building, some electricity, and a blank sheet of paper, and we can create everything within it.”

Our take. This quote captures what makes NVDA different; a fully integrated hardware, networking, software, and CPU infrastructure provider, not just a chip maker. The memory bottleneck doesn't threaten NVIDIA; it validates the AI factory thesis that Jensen has been building toward for decades.

Conviction Corner

RIA Q&A on FFF's Role in a Portfolio

How is FFF constructed?

A. Our process screens approximately 6,000 US-listed companies down to roughly 1,000 Founder-Led, then to the 200 largest by free float market cap, then to our final 100. The process is approximately 80% rules-based and up to 20% discretionary, which allows us to apply 23 years of institutional equity research judgment to final portfolio construction. Position sizes are capped at 7.5%, and the portfolio reconstitutes quarterly.

We are an actively managed conviction portfolio of the 100 Founder-Led companies we believe are best positioned to compound wealth over the long term.

Macro Minutes

U.S. Economic Releases · U.S. Economic Releases · June 29–July 6

What We're Watching

Thu, Jul 2: June Nonfarm Payrolls.

The most important data point of the week prints a day early this year, ahead of the July 4th holiday. Consensus expects 110,000 jobs added, down from May's 172,000, with the unemployment rate holding at 4.3%. The figure markets will actually trade on is Average Hourly Earnings, expected at +3.5% year-over-year. A soft headline number paired with sticky wage growth is the uncomfortable combination for the Fed: not weak enough to justify a near-term cut, but not strong enough to dismiss labor market cooling either. For memory and AI infrastructure names, the read-through is more about rates than fundamentals. Hyperscaler capital expenditure plans are running on multi-year timelines that don't bend much with a single jobs print, but a market repricing of rate-cut odds can still move the entire group, FFF included, on the day.

Washington Wire

Seoul Treats Memory as a Strategic National Asset

“Speed is the only way to survive. ”

South Korean President Lee Jae Myung · June 29, 2026

Our take. That's Lee Jae Myung, speaking alongside the chairmen of Samsung and SK Hynix as he unveiled what amounts to the largest government-anchored semiconductor and AI investment program announced anywhere in 2026; north of $570 billion in near-term commitments and well over $1 trillion when longer-dated pledges are included. Export control discussions continue to touch advanced memory and packaging technology alongside GPUs, since high-bandwidth memory is now considered as strategically sensitive as the chips it feeds. Any policy shift here would ripple through the entire AI supply chain. The government is treating memory as a strategic national asset. When a head of state is personally announcing fab buildouts alongside the chairmen of the two companies that control roughly 80% of global HBM (high-bandwidth memory) production, that's a signal the supply constraint is expected to persist. It's also a reminder of how concentrated this trade has become. Samsung and SK Hynix together make up roughly half of South Korea's KOSPI (Korea Composite Stock Price Index), and Seoul is now doubling down on the exact two stocks that already dominate its market, which raises the stakes on both the upside and the downside of that bet.

Not investment advice. Past performance does not guarantee future results. Investors should carefully consider FFF's investment objectives, risks, charges, and expenses before investing. The prospectus contains this and other important information. Read it carefully before investing at: FounderETFs.com/FFF Distributed by Vigilant Distributors, LLC.

The data presented reflects Founder-Led company weightings as of 5/28/26 and is subject to change without notice. Founder-Led weighting is determined by if a company's original Founder currently serves as a chief officer (e.g. CEO, CTO).

Comparison to other ETFs (VGT, IWF, VUG, XLK, QQQ, IVV, SPY, SPYM, VTI, VOO, IJH, VTV) is for informational purposes only and does not imply that FFF will outperform any listed fund. Different ETFs have different investment objectives, strategies, risks, charges, and expenses. Holdings and weightings change frequently and may differ materially at the time of reading.

A higher concentration in Founder-Led companies does not guarantee superior performance and may introduce additional risks, including key-person risk, governance risk, and concentration risk. Not a solicitation to buy or sell any security.

Founder Factor · Weekly Newsletter