Founders Solve the Unsolvable

This week we turn to biotech, and to the Founder who treated 'undruggable' as a starting point, not a verdict: Mark Goldsmith of Revolution Medicines (RVMD). We also revisit a cautionary tale, the first Founder-Led ETF and why it didn't survive, and flag the stat of the week: the heaviest AI spenders grew entry-level headcount 12%, not cut it.

Announcement

We are pleased to announce that Lauren Cassidy, CFA has been named Chief Investment Officer of the Founders 100 ETF (FFF), effective July 1, 2026. A 23-year institutional veteran, Lauren brings deep fundamental rigor and disciplined process to the strategy as she partners with Founder & CEO Michael Monaghan to lead a high-conviction portfolio of Founder-Led companies.

The idea for Founder ETFs was born in our nation's capital. While visiting the Smithsonian, Michael and Lauren stood in awe before the Great Garrison Flag, the same broad stripes and bright stars that inspired Francis Scott Key to write our national anthem after the battle of Fort McHenry. In that moment, they reflected on how the same spirit of freedom, grit, and courage that founded America continues to drive the founders building exceptional companies today.

That question led them to Bain & Company research showing that Founder-Led S&P 500 companies outperformed non-founder-led peers by 3.1x over 25 years and 2.1x over the following decade, yet most large ETFs own little of this powerful historical factor. They built FFF to close that gap and give investors meaningful exposure to Founder-Led businesses.

Lauren and Michael remain deeply aligned with shareholders as significant investors in the fund. Here's to the next 250 years of American grit, determination, and the Founders who carry that spirit forward.

Founder Spotlight

Dr. Mark Goldsmith at Revolution Medicines (RVMD)

Founder, President & CEO · Revolution Medicines (RVMD)

Dr. Goldsmith started Revolution Medicines because he believed patients with "undruggable" cancers deserved hope, not just time to say goodbye. His target was RAS, the on/off switch that tells healthy cells when to grow and when to stop. When RAS mutates, the switch gets stuck in the on position, and it now drives roughly 30% of all cancers, including about 90% of pancreatic cancers and a quarter to a third of lung and colorectal cancers. For decades, RAS proteins were considered untreatable because of their smooth surface, often compared to a golf ball, which left no place for a drug to grip.

His answer was daraxonrasib, a molecule that works like glue, binding to the mutated, active form of RAS and blocking the growth signal that keeps cancer cells dividing. This is the defining trait we look for in a Founder-Led company: a Founder who refuses to accept that a problem is unsolvable, and who spends the years it takes to prove otherwise.

What's the inflection?

In April, Revolution's Phase 3 pancreatic cancer trial doubled median overall survival, from 6.7 months on chemotherapy alone to more than 13 months on daraxonrasib, cutting the risk of death by roughly 60%. When the full data were presented at the ASCO Annual Meeting in May, the room of oncologists gave the results a standing ovation that lasted nearly a minute, including cheers and tears. Standing ovations are rare in medicine. When they happen, they tend to mark a real shift in the standard of care, and an inflection point in what investors should expect commercially.

The regulatory response has moved just as fast. On May 1, the FDA fast-tracked daraxonrasib and issued a "safe to proceed" letter, an unusual determination that lets pancreatic cancer patients access the drug early. Revolution decided to provide the drug free of charge ahead of formal FDA approval. The company also holds a National Priority Voucher, the FDA's newest mechanism for compressing review timelines, which we cover further in the Washington Wire below.

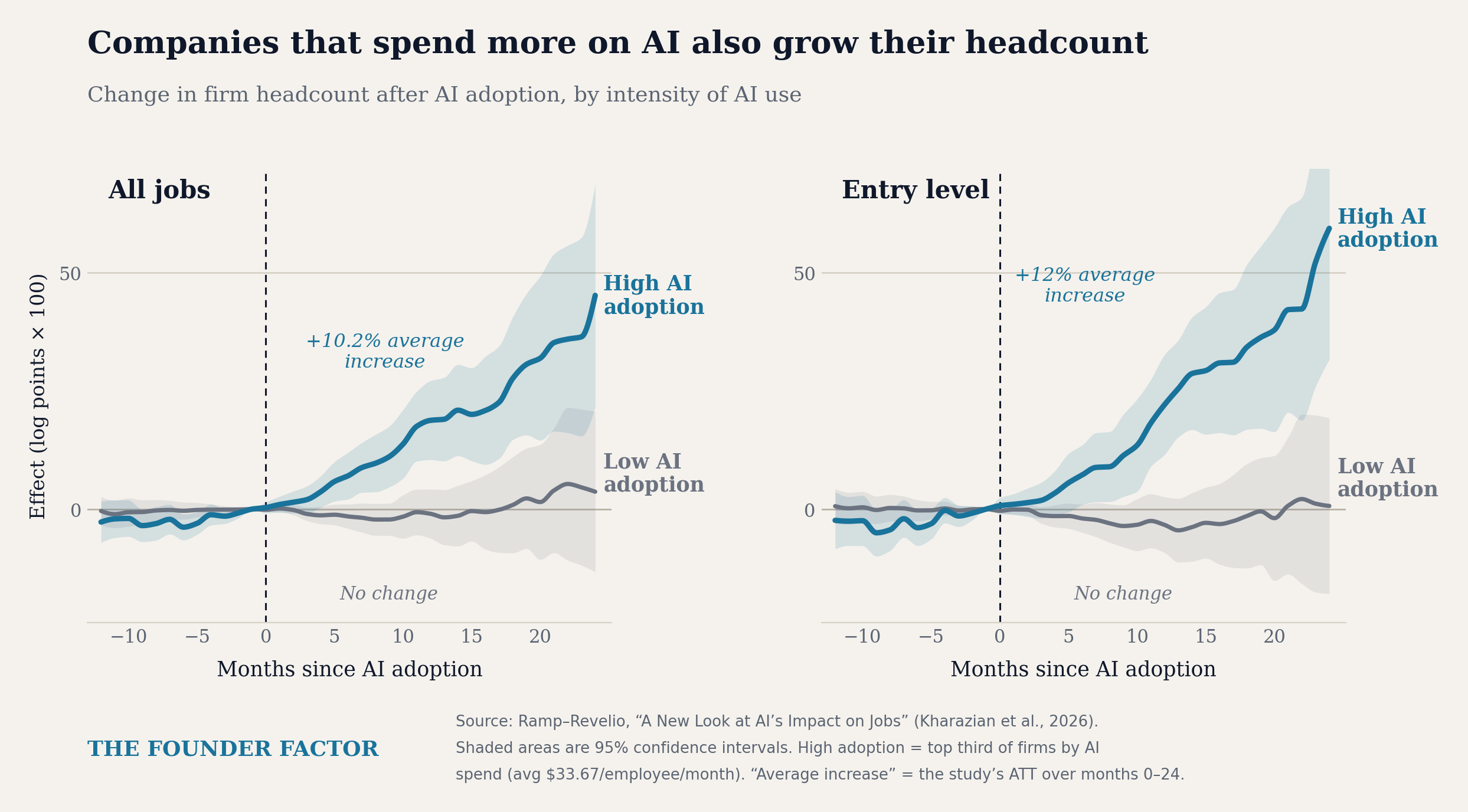

A Stat That Travels

+12%

The heaviest AI spenders grew entry-level headcount 12% in the two years after adoption, while firms that barely used AI saw no change. Total headcount rose 10.2%. Far from replacing junior workers, the companies leaning hardest into AI are hiring more of them.

Special Feature: BOSS vs. FFF

Why the First "Founder" ETF Failed & Why We're Different

Global X launched the Founder-Run Companies ETF, ticker BOSS, in 2017. The concept was sound: buy the largest 100 US companies where a Founder serves as CEO. By November 2023, it liquidated with less than $7 million in assets under management after six years on the shelf.

What went wrong

- Equal-weighted at roughly 1% each. A 100-name equal-weight book leaves no room for conviction. Winners got capped at the same size as laggards, every year, by construction.

- Founder departures took up to a year to trigger a sale. The index rebalanced annually, so a company could lose its Founder in January and stay in the fund through December.

- No fundamental screen. Inclusion was purely mechanical: the 100 largest Founder-run companies by market cap without any judgment on business quality based on recent earnings releases, balance sheet health, capital discipline, or valuation. Instead of being a flight-to-quality beneficiary during the 2022 Tech Wreck, BOSS owned many meme stocks that underperformed.

- Missed Founder-CTOs entirely. The index required the Founder to serve as current CEO. Founders who served in technical roles such as CTO, CSO, or CMO were excluded despite their daily leadership.

The result was a fund that looked the part but could not deliver.

What we built instead

- High-conviction weights up to 7.5%. FFF winners are allowed to run within a disciplined cap, not flattened to the same small size as every other stock.

- A fundamental overlay. FFF owns 100 of the 200 largest Founder-led stocks based on fundamental strength including income statement, balance sheet, cash flow, and valuation metrics, excluding lower-quality companies.

- Founder leaves? We sell. When Torstein Hagen announced May 14th he was stepping down as CEO after more than thirty years at the helm of Viking Holdings, we sold the stock one week later.

- Quarterly reconstitution. We re-evaluate what we own every quarter based on the freshest earnings season data. Our rules-based framework promotes disciplined decision-making by reducing emotional bias across market cycles. At market highs, it helps us counter overconfidence, trend extrapolation, and excessive risk-taking driven by greed and exuberance. At market lows, it helps prevent panic selling, short-term thinking, and deviation from the fundamental research process amid fear and loss aversion.

- Principal ownership with a 30-year horizon. Michael and I are among the fund's top shareholders. This isn't a sub-advisory mandate; this is how we invest for ourselves.

Being Founder-Led was never the whole idea. Having high-conviction weights of higher-quality companies with a Founder at the helm today was it.

Industry Insight

The Regulatory Fast Lane

Biotech's regulatory environment is quietly becoming a bigger part of the Founder story than most generalist investors appreciate. The FDA's Commissioner's National Priority Voucher program, launched last year, is designed to compress review timelines for drugs that address a critical national health priority from the usual 10 to 12 months down to as little as 1 to 2 months. As of May, the agency had granted its seventh approval under the pilot. Revolution Medicines intends to submit its own application under this program, which, combined with the "safe to proceed" letter it already holds, gives it a plausible path to one of the fastest approvals in oncology history.

The Founder-Led pattern shows up elsewhere in the portfolio's biotech sleeve too. Kymera Therapeutics, founded and still run by Dr. Nello Mainolfi, builds oral medicines that degrade disease-causing proteins rather than merely blocking them. This week an analyst upgrade cited an accelerated Phase 2b timeline for its lead asthma and eczema candidate, KT-621, now expected to read out by year-end rather than mid-2027. It is a smaller position than Revolution, but the same underlying thesis: a Scientist-Founder who stayed close to the platform long enough to compress years of clinical uncertainty into a single, near-term catalyst.

FFF is not a biotech fund, but it owns a meaningful bench of Founder-Led names across oncology, immunology, and life sciences tools. As of July 5, 2026:

| Company | Ticker | Founder | Weight |

|---|---|---|---|

| Revolution Medicines | RVMD | Mark Goldsmith | 0.88% |

| Royalty Pharma | RPRX | Pablo Legorreta | 0.73% |

| United Therapeutics | UTHR | Martine Rothblatt | 0.51% |

| Guardant Health | GH | Helmy Eltoukhy | 0.50% |

| BridgeBio Pharma | BBIO | Neil Kumar | 0.32% |

| Krystal Biotech | KRYS | Suma & Krish Krishnan | 0.21% |

| Corcept Therapeutics | CORT | Joseph Belanoff | 0.19% |

| Kymera Therapeutics | KYMR | Nello Mainolfi | 0.16% |

| Twist Bioscience | TWST | Emily Leproust | 0.13% |

| CG Oncology | CGON | Arthur Kuan | 0.12% |

| Kiniksa Pharmaceuticals | KNSA | Sanj Patel | 0.11% |

| Viking Therapeutics | VKTX | Brian Lian | 0.10% |

These 12 biotechnology companies make up ~3.96% of the total FFF portfolio. No single one is large enough on its own to move the fund, but combined they represent our conviction that the same pattern driving returns in AI infrastructure and capital markets — a Founder who takes on the most challenging technical problems in their field — shows up as clearly in a Phase 3 readout as it does in a data center buildout.

Portfolio Pulse

Founders in Their Own Words

“In retrospect, the trajectory of the agentic development over at least the last four months hasn't really accelerated in the way that we expected… our bets on the new structure haven't come to fruition yet. But I expect more significant AI benefits within the next three to six months.”

Our take. Even Meta is hitting the classic AI execution wall. The aggressive restructuring to chase agents is proving messier and slower than planned, but Zuckerberg's explicit 3–6 month timeline shows he still sees a clear line to real ROI. This highlights both the near-term friction and the optionality still embedded in the largest AI spenders.

“Something has gone completely wrong [with how AI is being sold to enterprises]… the basic view is I'm going to chillax and waste my time with tokens, I'm going to get no value, and they're going to get my IP… What aligns me with Nvidia… is control over their compute, their models, their data stack, and their alpha. They want to know they own the means of production.”

Our take. Karp is drawing a sharp line between generic AI output and creating value with insights and expertise. Palantir insists that customers own, control, and protect their data instead of generating "AI slop" and leaking their intellectual property. This view aligns tightly with the broader shift toward sovereign, high-stakes AI deployments where the platform that delivers real outcomes, not just output, wins.

Conviction Corner

RIA Q&A on FFF's Role in a Portfolio

Q. Does a Founder have to be CEO?

A. No, a Founder in the Founders 100 ETF may serve in any active chief executive role. Our fund includes Founders who serve as a Chief Executive Officer (CEO), Chief Technology Officer (CTO), Chief Medical Officer (CMO), Chief Scientific Officer (CSO), and similar roles. A Founder Chairman or Director is excluded because they are not running operations on a daily basis.

Washington Wire

“The world is a better, safer, healthier, and more prosperous place when the United States and its allies continue to lead in biotechnology.”

Bio Rad Laboratories CEO John F. Crowley

Our take. It is urgent that the United States remains a leader in biotechnology, through AI adoption, faster clinical research and trials, and regulatory review for approval. The FDA needs reforms to remain the "gold standard" while outpacing global rivals like China.

Not investment advice. Past performance does not guarantee future results. Investors should carefully consider FFF's investment objectives, risks, charges, and expenses before investing. The prospectus contains this and other important information. Read it carefully before investing at: FounderETFs.com/FFF Distributed by Vigilant Distributors, LLC.

The data presented reflects Founder-Led company weightings as of 5/28/26 and is subject to change without notice. Founder-Led weighting is determined by if a company's original Founder currently serves as a chief officer (e.g. CEO, CTO).

Comparison to other ETFs (VGT, IWF, VUG, XLK, QQQ, IVV, SPY, SPYM, VTI, VOO, IJH, VTV) is for informational purposes only and does not imply that FFF will outperform any listed fund. Different ETFs have different investment objectives, strategies, risks, charges, and expenses. Holdings and weightings change frequently and may differ materially at the time of reading.

A higher concentration in Founder-Led companies does not guarantee superior performance and may introduce additional risks, including key-person risk, governance risk, and concentration risk. Not a solicitation to buy or sell any security.

Founder Factor · Weekly Newsletter