The Great Sorting Begins

Earnings season opens with reports from the money center banks, Goldman, and the CPI print on Tuesday, as well as BlackRock and Morgan Stanley on Wednesday. We spotlight Founder Larry Fink of BlackRock this week just as private credit fears meet reality. Inside this issue, you'll find our Q2 Financials preview, why we think the private credit controversy is overblown, the CPI setup for Kevin Warsh's Fed, and our full Founders earnings season calendar on the last page.

Opening Bell

Welcome! At Founder ETFs, we help RIAs close the Founder Gap hiding in their clients' portfolios.

Founder-Led S&P stocks outperformed non-founder-led: 3.1x over 25 years and 2.1x over 10 years, according to Bain & Company. Yet our research shows the 300 largest US equity ETFs (90% category AUM) own just 12.55% Founders. We built the Founders 100 ETF (100% Founders) to close that gap.

Michael and I aren't a faceless asset manager. When you call, email, or text, you get us.

We're your partners: sharing our fundamental research, our highest-conviction Founder ideas, and following our disciplined, 80%+ rules-based process designed to help remove emotional decision making during periods of fear and greed. As two of the largest $FFF shareholders, we plan to be fully invested alongside you for the next 30 years. Your success is our success.

Earnings season is the great sorting mechanism. Macro narratives step aside, and numbers take center stage. FFF reconstitutes quarterly following earnings season precisely because we want the freshest fundamental data driving every position, not sentiment, momentum, or emotion. We enter this earnings season the way we always have: positioned by our process, patient, and watching our 100 Founders report one by one. The full calendar is on the back page.

We are here to answer your questions. Welcome to Issue #9.

Michael & Lauren

Founder Spotlight

Larry Fink at BlackRock (BLK)

Founder, Chairman & CEO · BlackRock (BLK)

Larry Fink founded BlackRock in 1988 with seven partners and one vision: that risk management, not product sales, should be central to asset management. Nearly four decades later, BlackRock is the largest asset manager in the world, still led by one of the premier capital allocators in financial services. BlackRock combines industry-leading scale, durable organic growth, expanding higher-fee businesses, and significant operating leverage, supporting continued double-digit EPS growth and a premium valuation.

We believe BlackRock is well positioned to deliver durable double-digit EPS growth, supported by industry-leading ETF flows, accelerating private markets and technology revenue, operating leverage, and continued capital deployment. Our $1,365 price target is based on a 21x P/E multiple on our 2027 adjusted EPS estimate of $62, implying ~31% upside.

The core of the thesis is organic AUM growth. BlackRock manages more than $13 trillion of client assets and continues to capture a disproportionate share of global ETF flows through iShares, the industry's leading ETF franchise. ETF adoption remains a secular tailwind as investors continue shifting assets to lower-cost solutions. BlackRock's scale, distribution, and product breadth position it to continue taking share.

BlackRock generates meaningful earnings growth despite an average fee rate of ~18 basis points. While modest, average fees are earned on one of the industry's largest asset bases, creating substantial operating leverage. Incremental AUM carries high margins, allowing earnings to compound faster than revenue over time.

We also see a multi-year opportunity from the expansion of BlackRock's alternatives platform. The acquisitions of Global Infrastructure Partners (GIP), HPS Investment Partners, and Preqin diversify revenue toward higher-fee businesses including infrastructure, private credit, and private markets data. Management expects these businesses to improve BlackRock's long-term organic growth profile while supporting margin expansion.

Technology remains another differentiator. Aladdin has become the leading portfolio and risk management platform for institutional investors, generating recurring revenue, deepening client relationships, and increasing switching costs. Combined with BlackRock's broad investment platform, technology enhances client retention and creates additional cross-selling opportunities.

Capital allocation provides an additional tailwind. Strong free cash flow supports ongoing share repurchases while preserving flexibility for acquisitions that strengthen BlackRock's competitive position and broaden its addressable market.

Risks We're Watching

Risks include prolonged concern about private market credit, U.S. or European equity market weakness reducing AUM, slower-than-expected ETF inflows, fee compression, weaker fundraising across alternatives, integration risk from recent acquisitions, and regulatory changes affecting the asset management industry.

A Stat That Travels

12.55%

Founder-Led S&P 500 index companies outperformed non-founder-led peers by 3.1x over 25 years and by 2.1x over 10 years, according to Bain & Company research. Yet the top 300 largest US equity ETFs (90% of category assets) own just 12.55% Founder-Led stocks in aggregate, according to Founder ETFs research.

3forC: Three Talking Points for Clients

This week your clients will ask about: 1) Banks, 2) Private Credit, and 3) Inflation. Let's dive in:

1) Banks

The money center banks — JPMorgan Chase (JPM), Bank of America (BAC), Citigroup (C), and Wells Fargo (WFC), plus Goldman Sachs (GS) — report Tuesday, and we get CPI. BlackRock (BLK) and Morgan Stanley (MS) report Wednesday. The banks disclosed low private credit exposure that calmed fears and drove an April rally in Financials. We think Q2 builds on that. We expect healthy loan growth and solid consumer and commercial credit trends across the board. We expect strong Capital Markets activity to favor JPMorgan over Bank of America. Capital Markets, our third largest GICS industry exposure, is firing on all cylinders. Trading revenue tends to benefit from high, but not extreme, volatility. Credit issuance has been solid, and new Founder-Led IPOs like SpaceX (SPCX) are adding to deal revenue, with Anthropic, Databricks, Anduril, and OpenAI IPOs next.

2) Private Credit

We believe the private credit "controversy" is overblown, and our Founders agree. We'll hear more from BlackRock's Founder Larry Fink on Wednesday, who said that private credit has zero similarities to 2007 and that institutional demand is accelerating even as retail pulls back. As an analyst covering Financials during the Great Financial Crisis, I speak from experience. This looks less like a credit crisis and more like the market repricing a specific corner of risk.

3) Inflation

The Fed will be watching Tuesday's CPI print closely. Headline inflation is expected to cool from 4.2% to 3.8% year over year, while core CPI, which excludes food and energy, should remain flat at 2.9%. A faster fall gives Kevin Warsh more room to cut rates later this year. A hot, "higher for longer" print would push that timeline out and weigh on stock and bond valuations.

Our Q2 earnings preview is what we expect, not what's guaranteed. Results can and will surprise.

Industry Insight

Capital Markets

Software and Semis get the headlines. Capital Markets, our third largest GICS industry exposure, has become one of the strongest fundamental stories in the portfolio.

The setup entering Q2 earnings is unusually favorable. Trading revenue tends to benefit from high, but not extreme, volatility, and the first half of 2026 delivered exactly that: an Iran conflict, a peace deal, a new Fed Chair, and the largest IPO in Wall Street history. Credit issuance has been solid all year, and the IPO window is not just open, it is Founder-Led: SpaceX (SPCX) priced in June, with Anthropic, Databricks, Anduril, and OpenAI slated for Founder IPOs in the next twelve months or so. Every one of those deals feeds fees to the Capital Markets complex.

Our Founder-Led Capital Markets and asset management names sit on both sides of this flow. BlackRock (BLK), Founder Larry Fink, gathers the assets and now owns a scaled private credit platform. Blackstone (BX), Founder Steve Schwarzman, and Apollo Global Management (APO), co-founder Marc Rowan, originate and manage the private capital the market keeps debating. Robinhood (HOOD), Founder Vlad Tenev, monetizes retail engagement with markets. Capital One (COF), Founder Richard Fairbank, extends consumer credit and is vertically integrating the Discover network to become a closed-loop network that, under the Volcker Rule, can offer unmatched rewards for debit card spending over time.

On private credit, specifically, our view is contrarian to the fear trade. The April bank disclosures showed money center exposure to private credit is low. Defaults have been concentrated in a specific corner of the market rather than spreading systemically. Institutional allocators are actually adding to their exposure, not retreating with retail clients. Having covered Financials through the Great Financial Crisis, I remember what genuine systemic stress looks like: exotic products stacking leverage on leverage, the absence of liquidity, and the inability to price risk. The current problem looks less like a credit crisis and more like a healthy marketplace repricing a specific area of risk.

On Tuesday, if the CPI print runs hot, then "higher for longer" rates will cool equity and debt valuations as well as deal activity.

Portfolio Pulse

Founders in Their Own Words

“The offers that you get for using the compute are so high that it may make sense.”

Our take. For a Founder who has spent >$100 billion on AI infrastructure this year, the comment reframes the large and growing AI capital expenditures, which have been heavily criticized by the Street. Our AI thesis is that the capex investments are creating long-lived assets that will generate positive free cash flow for decades to come. The value is not only in the chips and memory, but in the ecosystem.

“Only 62% of Americans have exposure to US stocks. I'd like to get that to 100%.”

Our take. Robinhood's founding purpose is "to democratize finance for all," which echoes our own vision at Founder ETFs "to fill the world with the peace, joy, and freedom of prosperity." Founders do not just aim to solve problems and build great products; many Founders work decades past achieving wealth to widen the circle of who shares in society's prosperity long term.

Conviction Corner

RIA Q&A on FFF's Role in a Portfolio

Q. My clients keep seeing private credit headlines. How much exposure does FFF have?

Limited. BlackRock (BLK), Blackstone (BX), and Apollo (APO) estimate they have up to $195 billion of combined distressed private credit exposure, equivalent to 1.2% of their >$16 trillion in combined assets under management (AUM). We estimate this is equivalent to 1.9% of combined trailing twelve months (TTM) net income, a manageable write-down if necessary. These three stocks make up just 8% of the portfolio. From our perspective, private credit risk is well contained and should normalize over the coming quarters.

| Est. Distressed AUM ($B) | Low | High | Total AUM | High % AUM | FFF Portfolio Wt. |

|---|---|---|---|---|---|

| BLK | 10 | 20 | 13,900 | 0.1% | 3.4% |

| BX | 30 | 50 | 1,300 | 3.8% | 3.5% |

| APO | 75 | 125 | 1,030 | 12.1% | 1.1% |

| Total | 115 | 195 | 16,230 | 1.2% | 8.0% |

To manage risk, no single position may exceed 7.5% at our quarterly reconstitution as each earnings season winds down. If the private credit story deteriorated, we would size down the holdings. Either way, our disciplined, 80%+ rules-based allocation helps us limit emotional decision-making during periods of fear and greed.

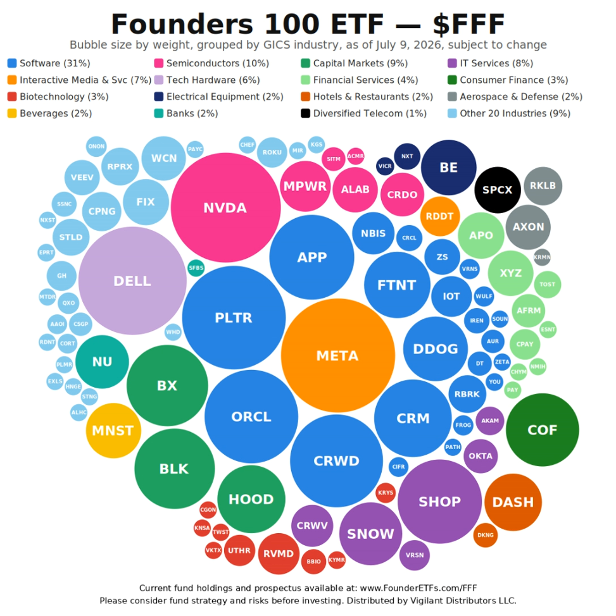

Founders 100 ETF ($FFF): bubble size by weight, grouped by GICS industry, as of July 9, 2026, subject to change. Current fund holdings and prospectus available at FounderETFs.com/FFF. Distributed by Vigilant Distributors LLC.

Macro Minutes

U.S. Economic Releases · Week of July 13

What We're Watching

Tue, July 14 - CPI (June reading)

CPI is the main event. Headline CPI is expected to fall from 4.2% to 3.8% year over year. Core CPI, which excludes food and energy, is expected to hold steady at 2.9%. The Strait of Hormuz reopening is doing the disinflationary work we outlined in Issue #5; this print is where it should start showing up.

Wed, July 15 - PPI (June) + Empire Manufacturing + Beige Book.

Producer prices are expected flat month over month after May's +1.1%, another energy unwind signal. The Beige Book gives Chair Warsh's Fed its anecdotal read ahead of the July FOMC meeting.

Thu, July 16 - Retail Sales (June) + Initial Jobless Claims.

Retail sales expected +0.3% headline with the control group at +0.5%, a read on whether falling gas prices are freeing up consumer wallets. Claims expected steady at 217k.

Fri, July 17 - Housing Starts + Industrial Production + University of Michigan Sentiment.

Housing starts expected to rebound +12.5% to 1,315k after May's slide. Michigan one-year inflation expectations, expected to ease from 4.6% to 4.4%, matter to a Fed watching whether the psychology of inflation is breaking alongside the data.

Our take. This is the most consequential macro week of the summer. If CPI confirms the post-peace-deal disinflation path, the case for a Warsh rate cut later this year strengthens, a constructive setup for growth equities. If the print runs hot, "higher for longer" compresses multiples. We think the energy math favors the cool print, but we position by process, not by prediction.

Earnings Edge

1 FFF Holding Reporting This Week

Larry Fink, Founder, Chairman & CEO

Before the Open · Wed, July 15

In Q2, Fink's commentary on private credit conditions will frame the debate for the rest of earnings season. We expect BLK to report strong Q2 '26 results, including fee growth toward the high end of management's 6–8% organic base fee growth framework, as strong ETF demand more than offsets any softness in institutional flows. We're also watching technology services growth as Aladdin extends further into private assets. Trading below its historical average P/E, the stock could see a double lift if Fink convinces the market that private credit concerns are overstated.

Washington Wire

“AI is going to make almost everything cost less. We're at the front end of a productivity boom. Economic growth won't be inflationary.”

Fed Chair Kevin Warsh

Our take. We believe the energy spike that drove headline inflation >4% will resolve once the war ends. Long term, we continue to share Warsh's view that as AI is fully incorporated into workflows, raising productivity, it will put downward pressure on prices, likely allowing the Federal Reserve to cut rates.

FFF Q2 Earnings Season July Calendar

Our Founders report over the next eight weeks. Here are the companies reporting in July. Dates are company-announced and subject to change:

| Company | Ticker | Founder Chief | Earnings Date | Weight |

|---|---|---|---|---|

| BlackRock | BLK | Larry Fink | 7/15 | 3.43% |

| ServisFirst Bancorp | SFBS | Tom Broughton | 7/20 | 0.09% |

| Steel Dynamics | STLD | Mark Millet | 7/20 | 0.69% |

| Capital One | COF | Richard Fairbank | 7/21 | 2.85% |

| Vicor | VICR | Patrizio Vinciarelli | 7/21 | 0.17% |

| Waste Connections | WCN | Ron Mittelstaedt | 7/22 | 0.99% |

| Essential Properties | EPRT | Peter Mavoides | 7/22 | 0.15% |

| Blackstone | BX | Stephen Schwarzman | 7/23 | 3.48% |

| Viking Therapeutics | VKTX | Brian Lian | 7/23 | 0.10% |

| SS&C Technologies | SSNC | Bill Stone | 7/23 | 0.32% |

| Verisign | VRSN | Jim Bidzos | 7/23 | 0.48% |

| Comfort Systems | FIX | Bill George | 7/24 | 1.13% |

| Bloom Energy | BE | KR Sridhar | 7/28 | 1.50% |

| ExlService | EXLS | Rohit Kapoor | 7/28 | 0.09% |

| Varonis Systems | VRNS | Yaki Faitelson | 7/28 | 0.21% |

| CoStar Group | CSGP | Andrew Florance | 7/28 | 0.26% |

| Robinhood | HOOD | Vlad Tenev | 7/29 | 2.31% |

| Kiniksa Pharmaceuticals | KNSA | Sanj Patel | 7/29 | 0.10% |

| Fortinet | FTNT | Ken Xie | 7/29 | 2.25% |

| Aurora Innovation | AUR | Chris Urmson | 7/29 | 0.29% |

| Meta | META | Mark Zuckerberg | 7/30 | 7.30% |

| RDDT | Steve Huffman | 7/30 | 0.81% | |

| Chefs' Warehouse | CHEF | Chris Pappas | 7/30 | 0.08% |

| Cactus | WHD | Scott Bender | 7/30 | 0.09% |

| Scorpio Tankers | STNG | Emanuele Lauro | 7/30 | 0.07% |

| NMI Holdings | NMIH | Brad Shuster | 7/30 | 0.07% |

| United Therapeutics | UTHR | Martine Rothblatt | 7/30 | 0.49% |

| Guardant Health | GH | Helmy Eltoukhy | 7/30 | 0.47% |

| Alignment Healthcare | ALHC | John Kao | 7/30 | 0.08% |

| Nextracker | NXT | Dan Shugar | 7/30 | 0.37% |

| IREN | IREN | Dan Roberts | 7/30 | 0.32% |

| Roku | ROKU | Anthony Wood | 7/31 | 0.47% |

| Corcept Therapeutics | CORT | Joseph Belanoff | 7/31 | 0.19% |

| Mirion Technologies | MIR | Thomas Logan | 7/31 | 0.10% |

| Monolithic Power Systems | MPWR | Michael Hsing | 7/31 | 1.34% |

Not investment advice. Past performance does not guarantee future results. Investors should carefully consider FFF's investment objectives, risks, charges, and expenses before investing. The prospectus contains this and other important information. Read it carefully before investing at: FounderETFs.com/FFF Distributed by Vigilant Distributors, LLC.

The data presented reflects Founder-Led company weightings as of 5/28/26 and is subject to change without notice. Founder-Led weighting is determined by if a company's original Founder currently serves as a chief officer (e.g. CEO, CTO).

Comparison to other ETFs (VGT, IWF, VUG, XLK, QQQ, IVV, SPY, SPYM, VTI, VOO, IJH, VTV) is for informational purposes only and does not imply that FFF will outperform any listed fund. Different ETFs have different investment objectives, strategies, risks, charges, and expenses. Holdings and weightings change frequently and may differ materially at the time of reading.

A higher concentration in Founder-Led companies does not guarantee superior performance and may introduce additional risks, including key-person risk, governance risk, and concentration risk. Not a solicitation to buy or sell any security.

Founder Factor · Weekly Newsletter